Your Exit Payout Scenarios

Weighing immediate cash, enhanced valuation multiples, and retained equity stakes

You’ve sacrificed a lot to build your SaaS business — late nights, missed life events, and carried the weight of every decision, every dollar, and every customer's problem.

Now, with acquisition offers on the table, the next chapter looms: cash out now, hold out for a bigger multiple, or keep some skin in the game?

The exit landscape is a maze of deal structures and trade-offs. Let’s break down your options so you negotiate with clarity.

Was this email forwarded to you? Subscribe here

Today's Note

Not all exits are created equal: your payout, risk, and future involvement hinge on the deal structure you choose.

All cash up front usually means a clean break, but less upside; deferring some payout or rolling equity keeps you in the game for a bigger win - if the business delivers.

Know your priorities - liquidity, valuation, or partnership - and negotiate from a position of clarity, not confusion.

Before we dive in, let’s set the guardrails. This isn’t a “what’s my SaaS worth?” playbook - there are entire industries (and plenty of other great resources) dedicated to that. I’m happy to sign an NDA if you want to discuss specifics.

I’m also not mapping out the full A-to-Z of selling your business, nor are we dissecting every nuanced financing structure.

Instead, we’re zeroing in on the most common SaaS deal structures and the practical trade-offs founders actually face, so you’re equipped to make sharper, more confident decisions when the time is right to exit.

Play around with the model I whipped up for this letter

The Exit Options

Let’s get to the point. For bootstrapped SaaS founders, valuation boils down to one core equation: ARR × Purchase Multiple = Valuation.

ARR represents predictable subscription income, while purchase multiples typically range from 3x to 5x for lower middle market SaaS businesses. This multiple hinges on growth rate, customer churn, profitability, market trends, and more.

When it comes to deal structures, buyers use a few key building blocks:

Buyer Equity1: The buyer’s own cash or investment in the deal.

Senior Debt: A loan the buyer takes out to help pay you at closing.

Seller Note: A chunk of the purchase price you collect over time, with interest. Often, it’s interest-only payments for a few years, then a lump-sum (balloon) payout of the remaining principal at the end.

Rolled Equity1: You keep a minority ownership stake and share in future upside.

Earnout: Extra payments you get if the business hits certain growth targets after the sale.

Here are the three common deal structures we’ll break down next:

Option 1: Full Exit – All Cash Now, Clean Break

Structure: Senior debt + buyer equity.

Pros: Immediate liquidity (100% cash at close), no post-sale involvement.

Trade-offs: Buyers often discount valuations (lower multiples) due to the perceived risk of losing revenue after acquiring the business. Ideal if you’re ready to sever ties and prioritize certainty over upside.

Option 2: Structured Exit – Higher Multiple, Some Risk

Structure: Mix of cash, seller note, senior debt, and earnouts.

Pros: Buyers stretch valuations (higher headline multiples) by tying payouts to future performance.

Trade-offs: Less upfront cash; you’re incentivized to ensure the business thrives post-sale.

Option 3: Hybrid – Cash + Skin in the Game

Structure: Partial cash + senior debt + rolled equity/seller note.

Pros: Balances upfront cash with participation in future upside (e.g., acquisition resale, recap, or IPO).

Trade-offs: Requires trusting the buyer’s long-term vision and staying involved in the business (extent is negotiable). Maximizes total potential but ties your wealth to their leadership.

Each option comes with its own trade-offs: Do you want cash now, a bigger payout later, or a mix of both? Full exits are best if you want a clean break. Structured deals can mean more money if you’re willing to wait. Hybrids let you cash out while still sharing in future growth.

Up next, we’ll exemplify how each works - and what your payoff would be under different scenarios

1A quick note on equity mechanics: Both buyer equity and rolled equity in these examples are modeled as participating preferred stock with an 8% preferred return, paid in kind (PIK). Translation: that 8% compounds as more equity, not cash in your pocket each year. Additionally, for simplicity, we’re showing gross returns only—no management fees, GP carry, or incentive equity in the mix. If you want to dig deeper, we’re happy to sign an NDA and walk you through how GP carry pools, management fees, and equity vesting schedules can shape real-world returns. Just reach out if you want to see how these details play out in practice.

Play around with the model we whipped up for this letter

Option #1: Full Exit - All Cash, All Done

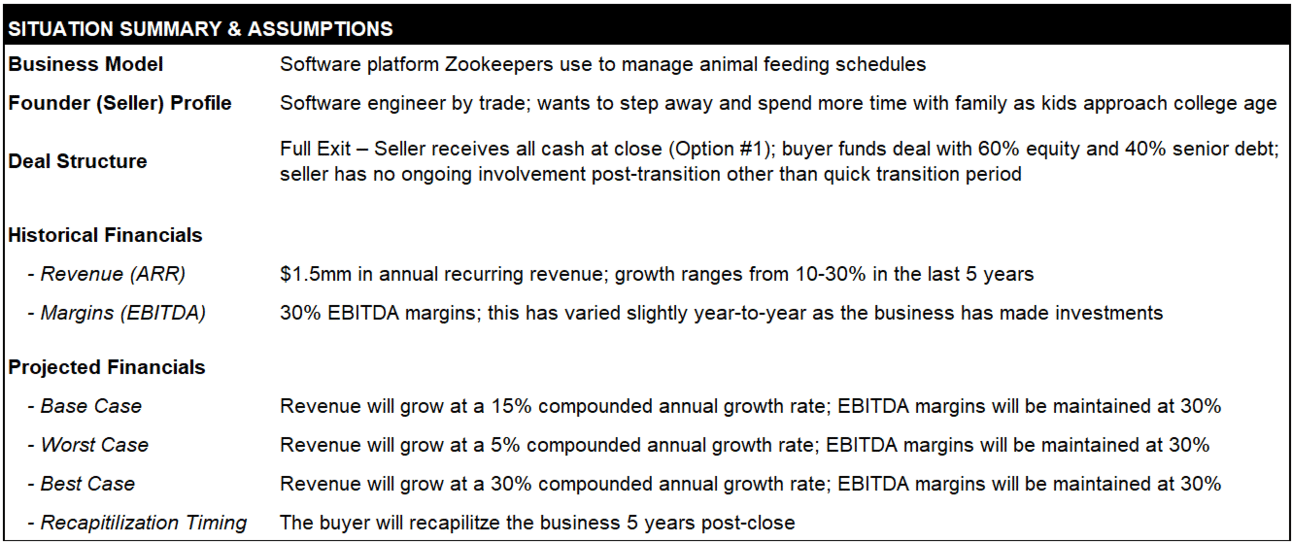

Let’s walk through a (very made up) example. Imagine a SaaS founder running a platform that helps zookeepers manage animal feeding schedules.

The business is humming along at $1.5M in ARR, growing steadily at 10–30% each year, with healthy 30% EBITDA margins.

The founder - a software engineer by trade - wants to step back and spend more time with his kids as they get older and college bills loom.

He chooses a structure that maximizes cash at close: Option #1. Here’s how it plays out:

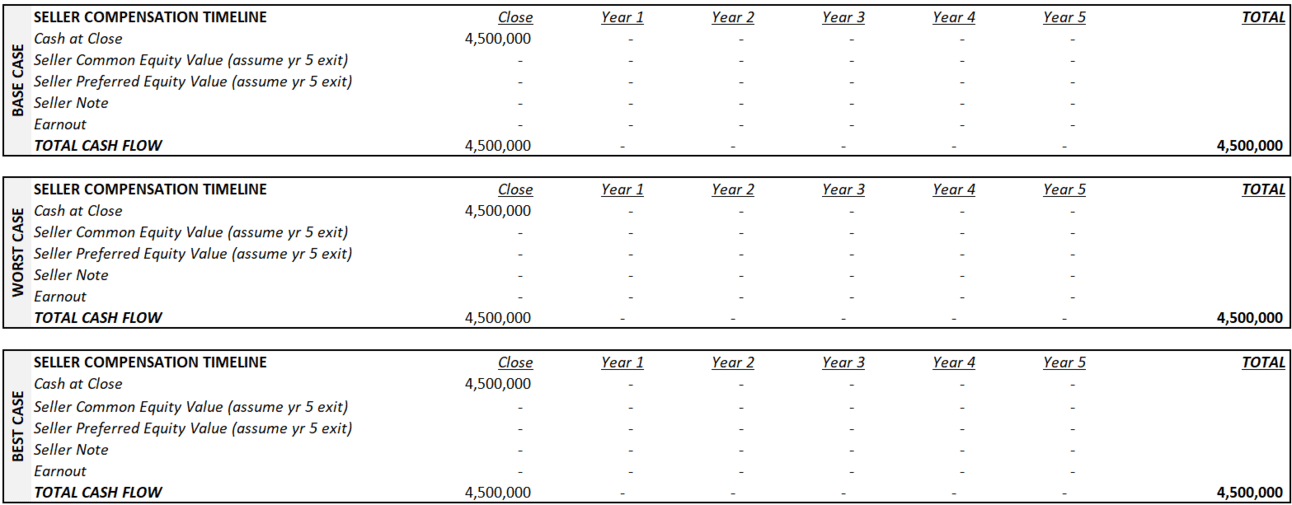

The buyer offers a 3x ARR multiple, so the purchase price is $4.5M.

On closing day, the seller gets $4.5M wired to his account-no earnouts, no notes, no future upside or risk.

The buyer funds the deal with 60% equity and 40% senior debt, and now owns all future upside (and risk).

Summary: This path is for founders who want immediate liquidity and a clean break. You get all your cash up front, walk away from the business, and can focus on your next chapter-no strings attached.

Play around with the model we whipped up for this letter

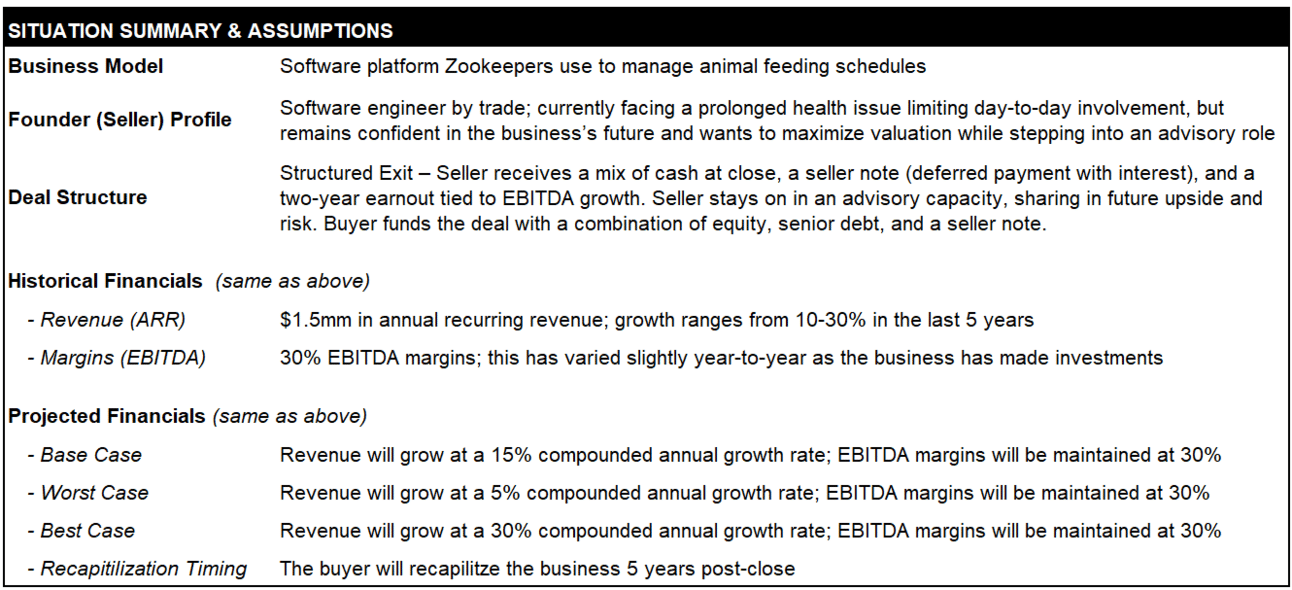

Option #2: Structured Exit – Maximize Valuation

Let’s run it back with our zookeeper SaaS, but this time the founder’s facing a curveball: a health issue that demands his focus and sidelines him from the day-to-day. Still, he’s bullish on the business’s staying power and wants to lock in a bigger valuation - even if it means deferring part of his payout and sticking around as an advisor.

Here’s how the deal shakes out:

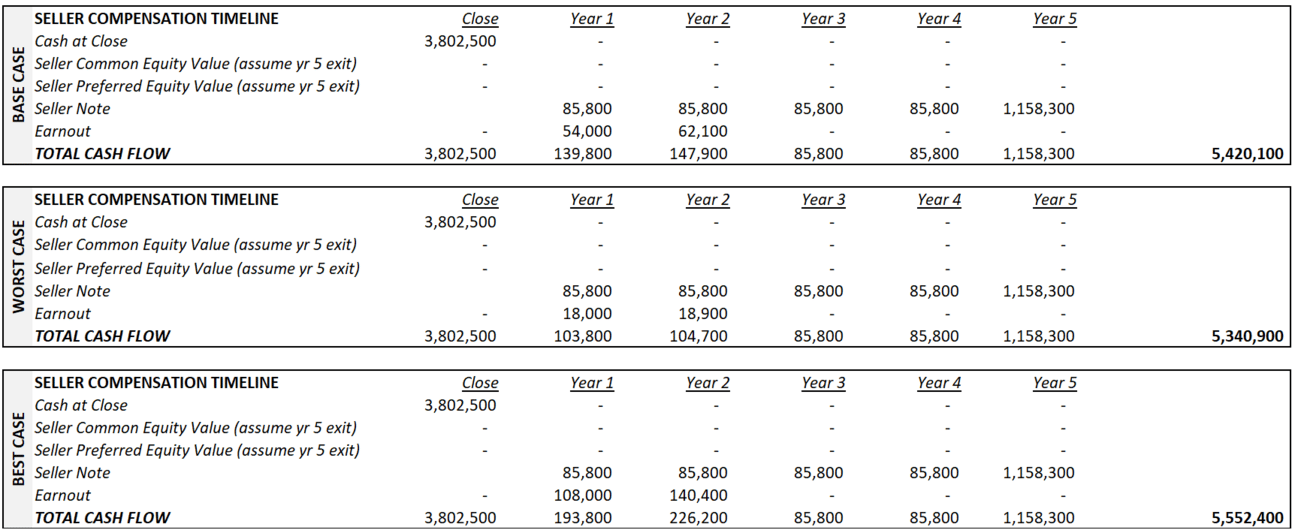

The buyer steps up with a 3.25x ARR multiple, landing the purchase price at $4.9M. At closing, the seller pockets $3.8M in cash, with another $1.1M structured as a seller note (an 8% loan to the buyer, with annual interest payments and a balloon payment of the remaining principal due at the end of year five or upon recapitalization).

To sweeten the pot, there’s a two-year earnout tied to EBITDA growth:

Hit the base case (15% annual EBITDA growth), and he pulls in $116K.

If the business crushes it (30% annual EBITDA growth), the earnout jumps to $250K.

If things underwhelm (5% annual EBITDA growth), the earnout drops to $35K.

Over the next five years, the seller collects steady interest payments from the note - roughly $86K per year. When the buyer recaps in year five, the seller gets the principal (about $1.1M).

Stack that with the earnout, and his total payout could surpass the headline price if the business delivers.

Summary: This setup lets the founder take real cash off the table now, swing for a bigger total payout if growth materializes, and still keep a seat at the table - all while stepping back from the grind.

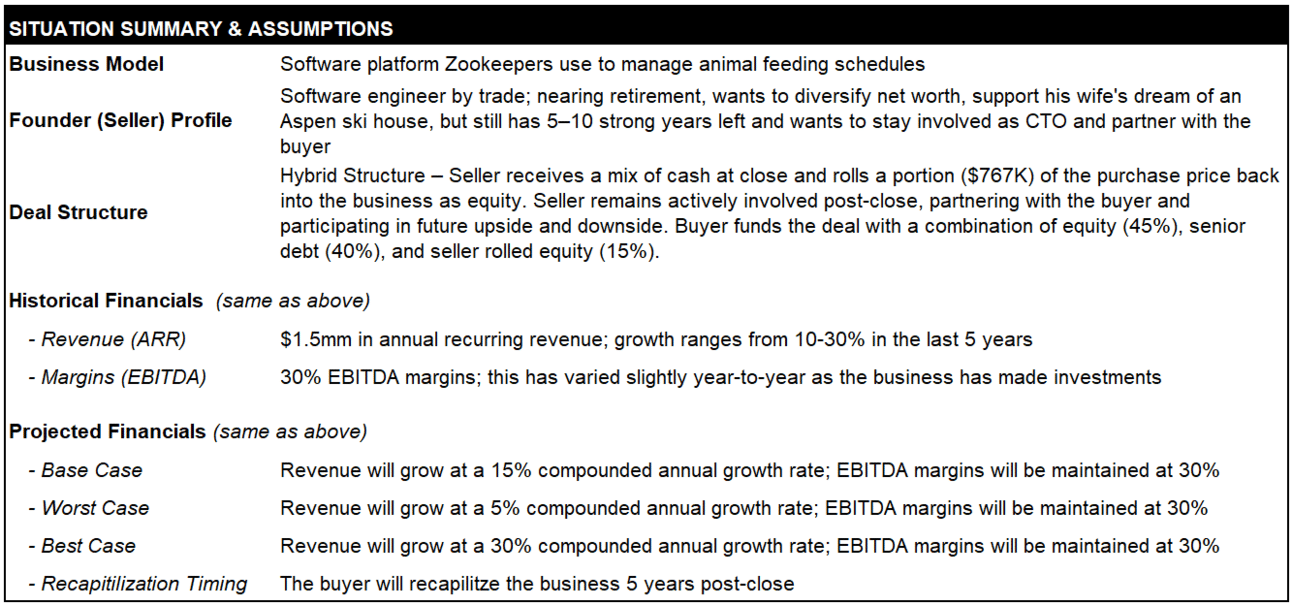

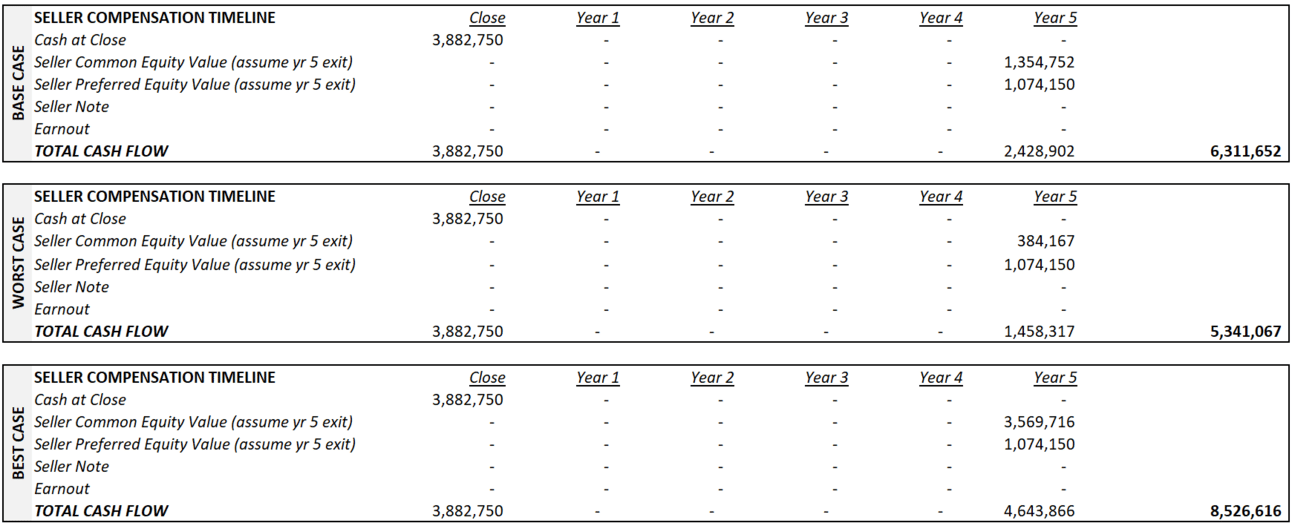

Option 3: Hybrid – Cash + Skin in the Game

Let’s revisit our zookeeper SaaS, but this time the founder’s eyeing retirement. Most of his net worth is locked in the business, his wife’s dreaming of that Aspen ski house, and he’s looking to diversify. Still, with 5–10 strong years left in the tank, he wants to keep some skin in the game and is genuinely excited to partner up as CTO with a buyer he believes in.

Here’s how the hybrid structure shakes out:

The headline number: 3.1x ARR, putting the purchase price at $4.65M.

At close, he takes home $3.9M in cash and rolls $770K back into the business as equity - giving him a real stake in the next chapter.

With that reinvested equity, he’s all-in on the upside (and the downside):

If the business grows at a base case (15% CAGR EBITDA over five years), his equity pays out $2.4M when they recap the business at year 5

If the business outperforms (30% CAGR EBITDA growth), he’s looking at $4.6M payout.

If it underperforms (5% CAGR EBITDA growth), the payout drops to $1.5M.

Summary: This structure lets the founder diversify, grab meaningful cash now, and still swing for a second big win alongside the new team - sharing in the upside (or downside) as the business evolves.

Navigating your SaaS exit isn’t just about chasing the highest number - it’s about structuring a deal that honors the years you’ve invested and sets you (and your team) up for what’s next.

Every decision at the table - cash, risk, and future upside - reflects the legacy you’ve built and the vision you hold for tomorrow.

Thanks for reading. As mentioned in my recent letter, it will take me some time to get this letter right. Please bear with me as I get my writing, rhythm, and cadence in order. Your feedback helps me get better with every issue.

Cheers to thoughtful exits and bold new chapters,

—Sanket

Clear breakdown of how the structure of a deal matters more than the headline number, especially when you start mapping risk vs upside over time